Welcome to our Bend Real Estate Market Update for the First Quarter of 2024. These statistics are for stick built homes on 1.0 acre or less in Bend zip codes 97701, 97702 and 97703 and do not include manufactured homes, condos, or townhomes. This report uses market data based on transactions that closed from January […]

In Central Oregon, brokers said Safeco – the state’s second largest insurer – as well as Progressive are effectively no longer writing new policies in certain ZIP codes in and around Bend, Sisters and Sunriver. One said Safeco is not writing new policies on properties over $1.5 million in Redmond, too.

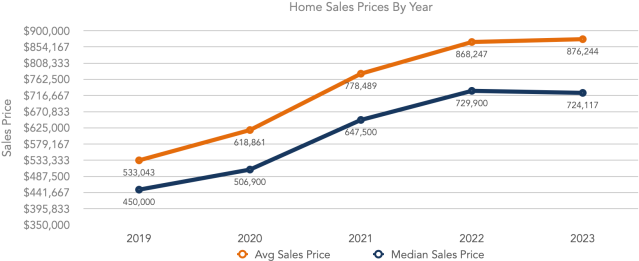

Welcome to our Bend Real Estate Market Update for the year 2023. These statistics are for stick built homes on 1.0 acre or less in Bend zip codes 97701, 97702, and 97703 and do not include manufactured homes, condos, or townhomes. This report uses market data based on transactions that closed from January 1 through […]

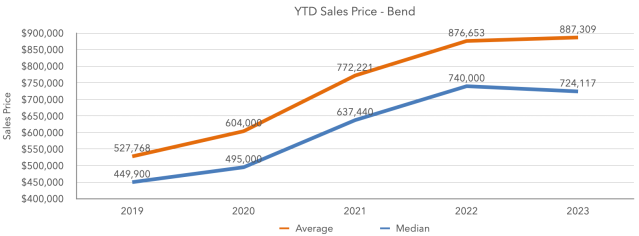

We saw a 20% reduction in inventory with pending sales and homes sold decreasing by 13% and 24%, respectively, attributed to high mortgage interest rates. Despite some uncertainty, Bend home values experienced a 1% increase in the average sales price ($887,309), with a slight decrease in the median price (2%). New construction represented a positive trend, accounting for 28% of listings and 22% of sales, with an median sales price of $740,000.

Buyers and sellers understandably have a lot of questions about the real estate market right now. While we don’t have a crystal ball, we do have the next best thing – 30+ years combined experience and educated local market insight, coupled with strong relationships with industry experts. These are our answers to the most common […]

While inventory has increased 77%, the number of homes sold is down about 32% from this time last year. The current mortgage interest rate is around 6.5% and this is the biggest hurdle for both buyers and sellers. Roughly 85% of homeowners with a mortgage have a rate under 5%.

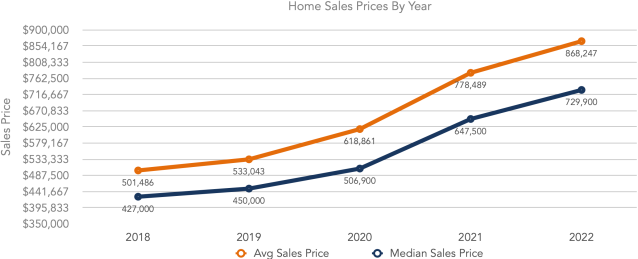

Bend, Oregon home values have come down since the peak of $775,000 in March 2022 but they are still up when compared to this time last year. The average sales price increased 11.53% to $868,247 and the median sales price increased 12.73% to $729,900. The median sales price at the start of 2022 was $740,000. It peaked at $775,000 in March and gradually started coming down to reach a low of $678,000 in December. Taking into account the highs and lows this year, the median sales price overall has settled at $729,900.

The December Beacon Report was published, which provides market insight for November 2022 and prior. According to the report, the median sales price for single family homes in Bend was $696,000 in November. That’s down from the market peak of $773,000 in March 2022 but up 1.9% from November 2021. In November 2020 and 2021, […]

Although inventory is up 52.24%, the number of pending sales and homes sold are down 23.8% and 13.12% respectively from this time last year. The mortgage interest rate is currently hovering around 7%, which has caused many buyers to pause and reassess their budget as this change has greatly impacted buying power and affordability, especially for first time buyers.

Sales prices are still increasing but days on market are a bit higher, price reductions are much more common and multiple offers are less common. It feels as if we are returning to a more normal and balanced market.

Welcome to our Bend Real Estate Market Update for the first quarter of 2022. These statistics are for stick built homes on 1.0 acre or less in Bend zip codes 97701, 97702 and 97703 and do not include manufactured homes, condos, or townhomes. This report uses market data based on transactions that closed from January […]

January of 2022 is on record as the most competitive month ever for homebuyers, according to data released Wednesday from Redfin. Seventy percent of home offers written by Redfin agents faced bidding wars in January on a seasonally adjusted basis, up from 67.7% in December and 61% in January 2021.

Income growth, the jobs recovery, demand for second and vacation homes, and strong in-migration into the region continue to fuel strong demand for housing. This past year saw some of the largest—if not the largest—home price appreciation on record. Any indicators of a market correction where prices will drop are difficult to find.

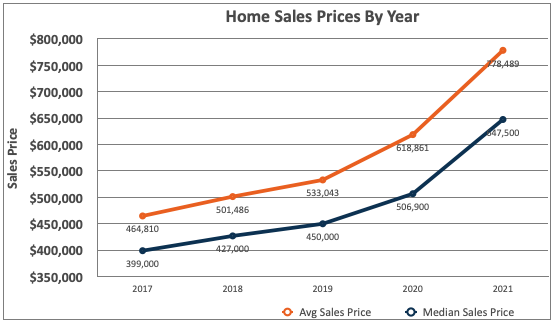

Bend’s median home price at the end of 2021 was $647,500. Home values have increased 42% since the onset of the pandemic. The combination of historically low inventory and high buyer demand has been the biggest driver of this increase.

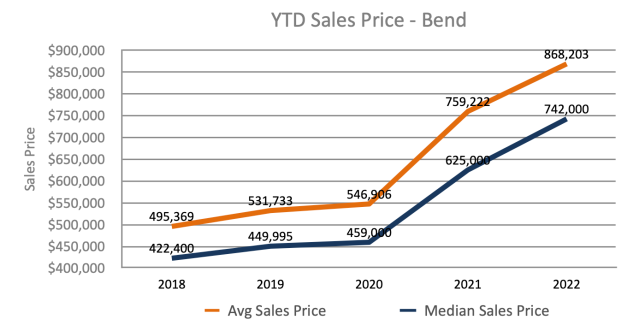

Compared to this time last year, the average sales price increased 27.85% to $772,221 and the median sales price increased 28.78% to $637,440.